According to the latest Zillow outlook, the US housing scene in 2026 is predicted to slowly find its balance again as borrowing costs start to ease a bit. Home prices are forecasted to finish the year nearly flat, rising around +0.9%, while existing home sales could see a mild uptick after a rather stagnant 2025. Honestly, this shift could signal a true turning point for the housing market in America after several taxing years of high interest rates and rising prices that made homeownership tough for millions.

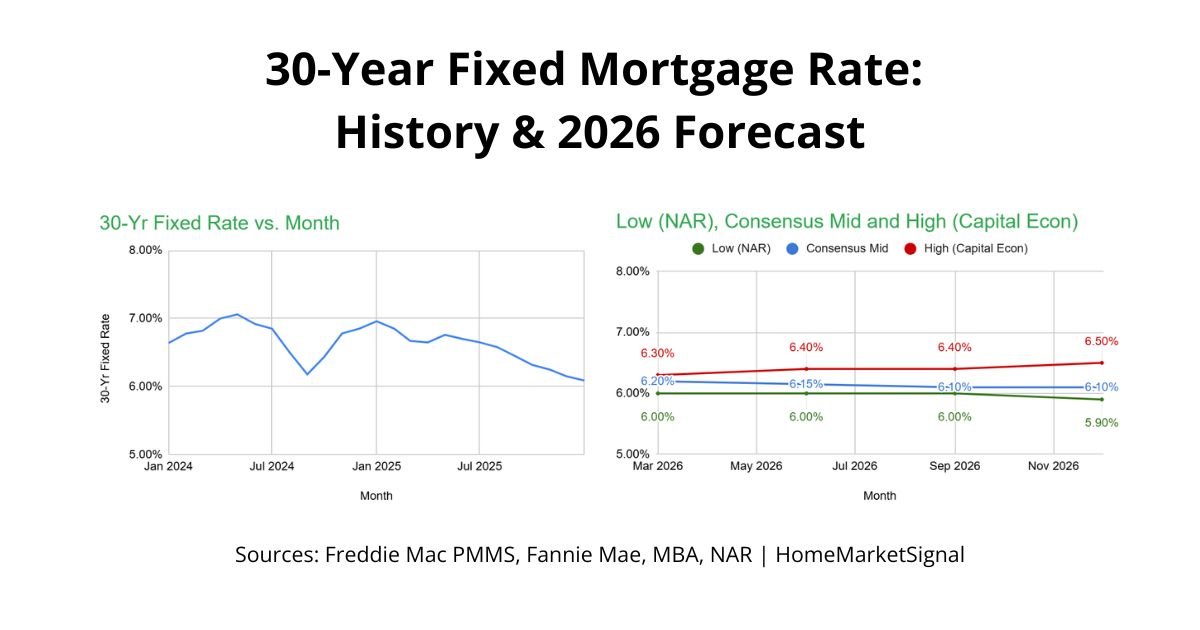

Fresh numbers are giving some hope to homebuyers and folks thinking about refinancing. The recent increase in mortgage applications comes as 30-year fixed mortgage rates dipped to 6.09% for the week ending February 12, as reported by Freddie Mac. That’s quite an improvement from the 6.87% average seen a year ago. In fact, this drop offers a welcome breather in a market that’s long been strained by hefty borrowing costs.

Latest Mortgage Rate Trends

Lately, the mortgage sector has been showing clear signs of revival, with application volume climbing 2.8% on a seasonally adjusted basis after three straight weeks of decline. Realtor.com attributes this rebound mostly to the rate reductions, which recently touched their lowest point in a month. Worth noting: that kind of small shift can really energize demand.

Joel Kan from the Mortgage Bankers Association mentioned that “mortgage rates moved lower with the 30-year fixed rate decreasing to 6.17 percent.” That dip gave refinancing activity a noticeable push, jumping 7% and now making up about 57.4% of all mortgage applications. The effective rate also edged down from the previous week, which helps homeowners lower their monthly payments in tangible ways.

This recent improvement in borrowing costs stems from several intertwined influences, including shifts in Treasury yields and cooling expectations around Federal Reserve policy. As noted in the Federal Reserve minutes, refinancing activity has stayed soft since previous rate levels remained higher than existing averages. But as rates start to ease, that pent-up demand is finally starting to move again.

2026 Forecast Breakdown

Home Value Projections

The 2026 forecast paints a picture less about explosive growth and more about stability. Zillow’s research expects home values to end that year up only about 0.9% on the Home Value Index (ZHVI). After years of rapid appreciation, this slower pace feels almost like a breather for the market.

This tempered growth pattern implies the housing sector is finding a more natural equilibrium after some wild swings. Buyers could hold greater sway at the bargaining table as fewer bidding wars and more realistic prices return. Simply put, the landscape might finally feel a bit fairer on both sides of the deal.

Existing Home Sales Volume

Existing home sales appear set for healthier momentum, with roughly 4.2 million transactions forecasted in 2026: that’s around a 3.9% increase from the year before. This rise shows how lower borrowing rates are unlocking demand from folks who sat idle through the higher-rate period. You might wonder: will this continue building through the year? Signs so far look positive.

The climb in transaction volumes also ties back to better affordability. Projections from Redfin suggest wages could finally grow faster than housing prices, which are only expected to rise about 1%. That shift between income and cost could make buying a home more realistic for more people across the country.

Factors Influencing Mortgage Rates

Federal Reserve Policy Impact

The Federal Reserve still plays the starring role when it comes to steering mortgage rate trends. According to recent FOMC minutes, delinquency rates remain near historical lows for most types of home loans, which points to fairly strong credit health overall. Naturally, how the Fed handles interest rates will heavily shape where mortgage rates head throughout 2026.

Investors are paying close attention to Treasury yields too, since those directly influence 30-year mortgage pricing. Because mortgage rates and Treasury yields tend to move hand-in-hand, any volatility in the bond market usually filters into mortgage quotes within a short stretch of time.

Economic Conditions and Inflation

Broader economic signals like inflation and job growth will keep tugging at mortgage rate fluctuations. The current forecasts lean on the expectation that inflation pressure will keep easing off, which would allow the Federal Reserve to stay on a friendlier footing regarding future rate moves. Think about it: lower inflation generally means more breathing space for borrowers.

The long-awaited housing reset that many analysts talk about still depends on these macro forces aligning. If inflation picks up again or economic performance falters, the rate outlook for 2026 could shift quickly. So while the outlook seems calm now, it’s not on autopilot.

Buyer and Seller Implications

Affordability Improvements

Thanks to easing mortgage rates and slower home price growth, affordability should gradually improve in 2026. If rates indeed land around the lower 6% range, monthly mortgage costs could start fitting household budgets a bit more comfortably. That’s encouraging news for those long priced out of the market.

Local professionals report that “seeing rates go down to about 6% has really brought more buyers into the market. If that trend continues or sticks, that’s going to definitely help.” Clearly, even small changes in rate perception can reignite buyer enthusiasm and restore confidence in making offers again.

Inventory and Market Balance

The housing market appears poised for a healthier equilibrium in 2026. More seasonal listings should expand buyer options, reducing the intense bidding battles seen in prior years. The outcome: buyers get time to think, compare, and decide smartly. That’s a welcome change of pace.

Meanwhile, sellers may need to recalibrate expectations because top-dollar, multiple-offer deals won’t be the norm anymore. Adapting to fairer pricing and longer market times will be part of adjusting to these more typical, balanced conditions. Real talk: it’s a shift toward normal, not a downturn.

Regional Variations and Market Dynamics

Although national data gives broad direction, 2026 will look quite different across regions. Various metro areas will respond uniquely, depending on local economies, job gains, and housing supply limits. The reality is: there’s no one-size-fits-all story in real estate.

Places with strong employment hubs and limited listings could still notice solid price growth, while cities with surplus housing or weaker job markets might see more cooling. Understanding those local dynamics will be key for both buyers and sellers hoping to make well-timed moves this year.

Refinancing Opportunities

Falling mortgage rates have sparked a new wave of refinancing: applications jumped 7% and now make up 57.4% of total mortgage activity. Homeowners who locked in loans above 7% now find solid chances to trim those monthly bills. It’s good timing, honestly.

This rise in refinance activity shows many households acting fast to capture savings, though the Federal Reserve cautions the overall volume still sits below normal levels. That’s because plenty of existing loans still carry lower rates than what’s offered today, keeping some homeowners on the sidelines.

Anyone considering refinancing should keep an eye on Treasury yields since they heavily influence the 30-year mortgage rate trends. For those above the current 6.09% mark noted lately, now might be the right window to act before markets shift again.

Expert Predictions and Market Outlook

Most industry voices maintain a cautiously upbeat tone about 2026. The collective expectation is that slower, steady declines in mortgage rates will gradually revive home sales without pushing prices back into unsustainable territory. Granted, that balance is delicate but promising.

According to Zillow, “persistently soft rent growth suggests renters will retain negotiating power while landlords face limited pricing momentum.” That balance could tilt the buy-versus-rent decision more toward ownership, giving home sales an extra boost as renting looks less advantageous.

Meanwhile, recent data from the mortgage bankers association shows effective rates continuing to slide week-over-week. That trend implies some durable momentum for lower lending costs. Still, experts remind us that global economic twists can quickly change the picture, so staying alert is crucial.

Long-term Market Implications

Looking further out, the 2026 forecast hints at a more sustainable era in housing if rates stabilize around the low-to-mid 6% mark. Such a level could provide a steady foundation for consistent activity rather than speculative spikes. Key point: predictability beats volatility.

The expected “reset” many analysts describe may usher in healthier long-term fundamentals, with steadier appreciation and affordability aligned closer to incomes. Sure, there might be short-term growing pains, but overall, this normalization could strengthen the housing system for the long haul.

Actionable Guidance for 2026

For those eyeing a purchase soon, there are strategic angles to consider. Locking in rates close to current lows could mean notable lifetime savings on your loan. Given that Freddie Mac just reported 6.09%, that margin could matter quite a bit down the road.

Buyers should anticipate mild gains in sales and a market with a bit more breathing space. With fewer bidding wars, people can take proper time to inspect and negotiate—something missing from the frenzy of past years.

Homeowners sitting on loans above 7% should do the math on refinancing options. The data showing 57.4% refinance share means plenty of peers already acted, so getting quotes now could be smart. Small savings can add up over time; experience shows that.

Sellers, on the other hand, may face a more strategy-driven market. Pricing accuracy and presentation will count more as competition balances out. The automatic “sold above list” days might be gone, but a well-prepped listing can still attract serious, motivated buyers.

Conclusion

Overall, the 2026 forecast for US mortgage rates signals gradual progress rather than dramatic swings. As rates ease toward the low 6% range, home sales should pick up moderately, while price growth remains restrained. The recent decline to 6.09% already hints at improving momentum across the board.

Combined trends like wage growth outpacing price increases and more available inventory point toward a steadier, more accessible housing environment. Naturally, there are still challenges, but signs suggest 2026 could mark a healthier, more sustainable era for the market.

Anyone planning to buy, sell, or refinance should continue watching rate movements closely. These better conditions won’t last forever, and acting timely could secure significant advantages. In practice, being informed remains the smartest move for achieving solid results.