Over the years of studying the housing market, I’ve kept a close eye on how mortgage rates shift and how that movement touches both buyers and sellers. Now, as 2026 unfolds, one big question keeps popping up in almost every chat with people dreaming of owning a home: will this be the year mortgage rates finally drop? Well, the most recent projections coming from top financial analysts point to a kind of careful optimism; rates might just ease down steadily through the rest of 2026.

At this moment, the data shows the 30-year fixed mortgage rate standing at 6.27% as of March 18, 2026, according to Bankrate. Meanwhile, refinance rates have nudged a bit higher; the average for a 30-year fixed-rate refinance loan hit 6.55% as of March 24, 2026, based on insights from Zillow. It’s a modest uptick, yet worth noting for anyone watching the market closely.

Current Mortgage Rate Snapshot

Knowing where rates are sitting today offers vital context before predicting what’s next. The mortgage market has been pretty jumpy lately; rates have risen around a quarter of a percentage point in the past few weeks. That bump mirrors long-term interest rate moves, shaped partly by ongoing inflation pressures and fading expectations of Federal Reserve rate cuts.

As of March 2026, here’s what the current rates look like in a quick snapshot:

30-year fixed mortgage: 6.27%

30-year refinance rate: 6.55%

Average discount points: 0.33 points

These current figures build a tough environment for anyone aiming to buy. With the median existing home price pegged at $398,000 in February 2026 by the National Association of Realtors, a typical monthly principal and interest payment of $1,965 would eat up around 23% of a median family’s income. HUD’s 2025 data puts that family income at about $104,200… challenging proportions, no doubt.

Expert Forecasts for 2026: What Will Happen to Mortgage Rates in the Rest of 2026?

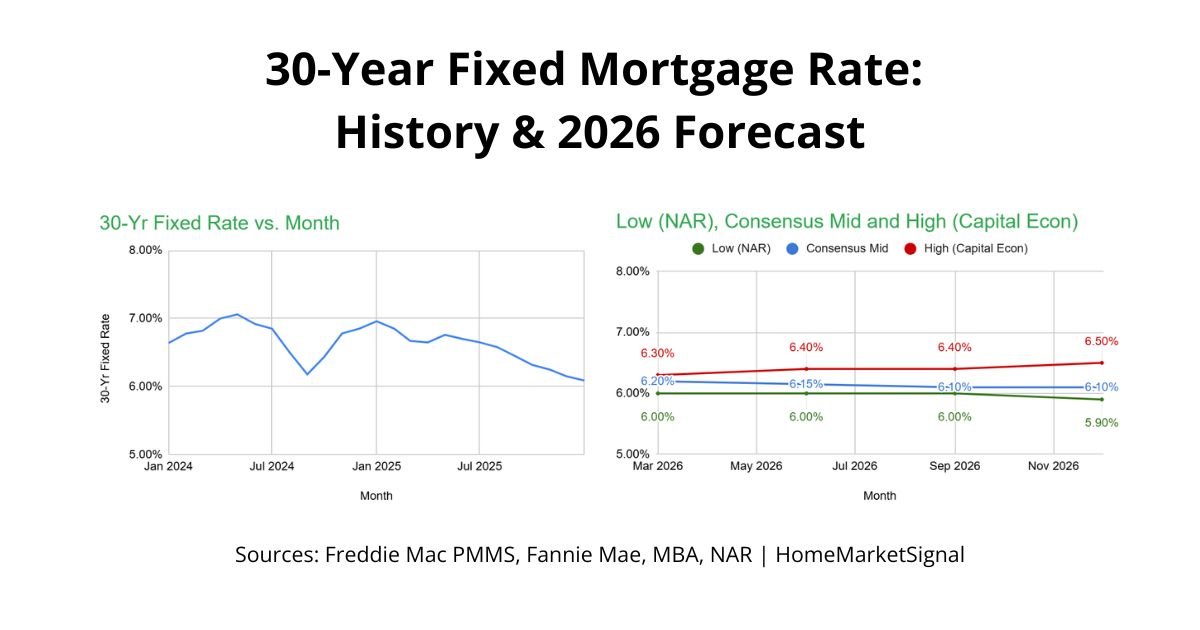

Among the most complete predictions, Fannie Mae’s March Housing Forecast paints a brighter picture than before. According to TheStreet, this new forecast is more upbeat than February’s, reflecting expectations that the economy will slow down a bit, easing rate pressures.

Quarterly Rate Projections

Through 2026, Fannie Mae projects a slow, steady drop in mortgage rates across the quarters:

Q1 2026: 6.0%

Q2 2026: 5.9%

Q3 2026: 5.8%

Q4 2026: 5.7%

This marks a noticeable improvement from February’s older estimate, which had both Q1 and Q2 pegged at 6.1%. The update signals shifting expectations tied to broader economic adjustments and, naturally, the evolving interest rate climate.

Still, the Mortgage Bankers Association leans a bit more cautious. Mike Fratantoni, their chief economist, recently noted that “Mortgage rates have moved up about a quarter percentage point in recent weeks as longer-term interest rates accounted for the increase in inflation and, hence, the reduction in the chance that Fed would cut further this year.” Their projection pegs 2026’s range between roughly 6% and 6.5%, and present patterns hint that outcomes might cluster on the higher end of that spectrum.

Key Economic Drivers Influencing Rate Direction

Several core economic forces will truly steer whether mortgage rates fall through the rest of 2026. Understanding these elements sheds light on why experts remain both hopeful and cautious at the same time. You might wonder which ones matter most: inflation, Fed policy, and general economic growth top the list.

Federal Reserve Policy Impact

As many expected, the Federal Reserve decided to keep its benchmark rate unchanged at the March 18, 2026 meeting. That decision underscores their careful stance amid ongoing concerns over stubborn inflation. Current projections even leave room for one more rate cut by the end of the year; but if inflation stays sticky, those cuts may not materialize.

The Fed’s benchmark rate does influence mortgage rates, although not one-to-one. Typically, when the Fed trims rates, it nudges mortgage rates lower as well, making home loans a bit easier on borrowers’ budgets. Simple cause and effect, though rarely exact.

GDP Growth and Economic Indicators

Weaker GDP growth often signals a softening economy, and that pattern historically drives mortgage rates downward. Fannie Mae’s March update relies in part on expectations of slower economic output, meaning policymakers may be pushed toward easing credit conditions to keep momentum alive. Worth noting: sluggish growth can pressure rates downward, yet it comes with trade-offs such as worries about jobs or income stability that affect homebuying confidence.

The push and pull between economic growth and mortgage rates creates a tricky balancing act. When growth drags, rates often dip, but consumer confidence can slip right along with it. It’s rarely a simple win for anyone.

10-Year Treasury Yield Correlation

The 10-year Treasury yield basically sets a kind of guiding star for mortgage rates; the two usually move in step. When Treasury yields fall, mortgage rates often follow suit. It’s why analysts watch this closely when predicting future rate cuts.

Lately, shifts in the Treasury market suggest investors are bracing for uncertainty. That mindset tends to support lower yields and, by extension, could help press mortgage rates lower as we move deeper into 2026.

Housing Market Impacts and Inventory Challenges

The way mortgage rates and housing market forces loop together creates a fascinating cycle. As borrowing costs move, they shape supply and demand in tandem. Looking at current conditions, several trends appear poised to define the remainder of this year. Key point: it’s about more than just rates; supply constraints are still pretty stubborn.

Construction and Housing Supply

Single-family housing starts are expected to dip about 6.2% year over year through the first three quarters of 2026, based on Fannie Mae’s projections. This slower pace of new builds tightens inventory further and stops prices from cooling too much, even as fewer buyers step up due to elevated borrowing costs.

The construction pullback says a lot about builder sentiment; with financing more expensive and demand uncertain, caution prevails. That said, Fannie Mae expects an upswing of around 5.1% in 2027 single-family starts. So perhaps this lull is just a pause rather than a prolonged slide.

Home Price Trends

On pricing, national averages show only a 1.3% climb in 2025—the weakest stretch since 2011 per S&P CoreLogic Case-Shiller data. Clearly, elevated mortgage rates took a bite out of affordability and curtailed buyer enthusiasm. You might say the fever finally broke, at least in part.

Interestingly, half of the 50 largest metropolitan areas actually saw price declines in the last year, according to Zillow‘s findings. That split helps explain how national averages mask a patchwork of results—some cities slipping modestly, others holding steady or even ticking upward due to resilient local economies.

Affordability and Market Access

When we crunch the numbers, affordability remains a brick wall for many would-be buyers. Median family income sits at around $104,200 versus a $398,000 median home, leaving a hefty payment ratio. For even middle-income households, that’s stretching the budget thin.

Now, if rates really do drop from 6.27% to the anticipated 5.7% by late 2026, the monthly savings could become meaningful. Lower interest means lower payments, and that could reopen the door to homeownership for folks who were recently priced out.

Regional Market Variations and Local Context

While national headlines grab attention, the lived reality depends on where you’re buying or selling. Each U.S. region plays by slightly different rules. Look, what happens in Phoenix might differ wildly from Boston or Detroit due to jobs, population flows, and local policies affecting housing supply.

The fact that 25 of the 50 biggest metro areas saw year-over-year price drops underscores the need to dig into local data rather than just broad summaries. High-growth cities might feel rising demand more sharply when rates fall, while slower economies could face longer recoveries even with friendlier mortgage numbers.

Areas enjoying strong job creation or migration trends could keep humming despite borrowing costs, whereas communities dealing with layoffs or economic contraction might hit headwinds faster as interest rates shift. Real talk—it’s not one-size-fits-all.

What Homebuyers and Sellers Should Do

Given all this, both buyers and sellers have tough calls to make. Strategy matters now more than ever. The goal: anticipate how shifting mortgage rates might hit your personal timing and financial setup… not easy, but possible with good information.

Buyer Strategies

Falling rates typically make homes cheaper to finance, lower monthly bills, and cut long-term interest spending. But buyers shouldn’t keep waiting forever for the “perfect” window because falling rates could push more people back into the market, rekindling price competition.

Here are a few approaches worth considering:

Rate Lock Strategies: If you’re actively searching, know the difference between discount and origination points. Discount points can squeeze your rate lower, while origination points are lender fees to originate and manage your loan. With the average hovering at 0.33 points, current rate-lowering costs remain moderate.

Market Timing: Sure, rates are expected to slip slightly, but more buyers chasing limited inventory could cancel out savings through steeper prices. Those with solid financial footing may prefer to act now rather than gamble on bigger dips later.

Refinancing Preparation: For current homeowners, meanwhile, it’s smart to keep tabs on mortgage movements. At 6.55% refinance rates, there’s definite room for savings if future forecasts play out and rates ease downward.

Seller Considerations

If you’re selling or considering it, brace for staying power in prices. While price growth has slowed, supply scarcity keeps pressure on valuations. For most of 2026, the market isn’t likely to crash; supply-demand tension persists.

That said, if rates fall as forecasters hope, buyer enthusiasm could rise again later in the year, potentially broadening your buyer pool. It’s a balancing act: patience might yield stronger offers, but well-priced listings today can still perform if they’re in desirable spots.

Risks and Economic Uncertainties

Even amid the rosy outlook, several wildcards could throw off projections. Being aware of these keeps expectations grounded. After all, markets can pivot faster than many think.

Inflation Pressures

Persistent inflation remains the biggest risk to lower-rate hopes. If consumer prices climb faster than expected, the Federal Reserve could feel pressure to maintain or even hike rates again, running directly opposite today’s predictions. Simply put, inflation is the troublemaker here.

Recent CPI data already nudged mortgage rates up about a quarter point as markets recalibrated around tighter Fed stances. Should inflation keep surprising upward, the easing many expect might stall entirely.

Geopolitical and Economic Shocks

External events, too, can rattle the system; what happens overseas often ripples into bond yields and, in turn, mortgage pricing. Following the February 27 Iran conflict, for instance, rate volatility ticked up according to Freddie Mac data, shaping April outlooks noticeably.

Such geopolitical disruptions tend to push investors toward safer assets, shifting bond patterns and influencing mortgage benchmarks. It’s the classic “flight to quality” scenario playing out in real time.

Economic Growth Surprises

Slow growth supports softer mortgage rates, but if the economy shows unexpected strength, the Fed may keep its foot on the brake longer, keeping borrowing costs elevated. Conversely, a sharper downturn could force quicker cuts, sending rates down faster than planned. So, swings either way remain possible—uncertainty still rules the day.

Looking Ahead: 2027 and Beyond

Many long-range models stretch into 2027, offering glimpses beyond this year’s turbulence. Fannie Mae is forecasting a 5.1% bump in single-family housing starts that year, signalling a comeback in building activity to ease inventory pressure. That outlook could spell steadier price movement and more balanced supply-demand conditions.

If housing construction rebounds and mortgage rates slide simultaneously, the result may finally be a more even market. Still, the scale and pace depend heavily on inflation, Fed choices, and consumer demand trends throughout late 2026. In short, we’re not out of the woods yet.

The handoff from Q4 2026 into 2027 will serve as a stress test for how sustainable these rate drops are. If underlying conditions keep aligning, borrowers entering 2027 might find a far friendlier mortgage landscape waiting for them.

Conclusion: Cautious Optimism for Rate Declines

So, when someone asks, will mortgage rates go down in 2026, the honest answer leans toward guarded optimism. Fannie Mae anticipates a fall from 6.0% in Q1 to 5.7% by year’s end, whereas the Mortgage Bankers Association keeps its cautious 6% to 6.5% target Ernstly aware of lingering volatility. Different shades of optimism, but optimism nonetheless.

Helping forces include softening GDP growth, possible Fed cuts, and fading inflation pressure. But global turbulence, surprise inflation, and stronger-than-expected economic figures could all rearrange the path. Forecasts come with fine print, always.

The takeaway for buyers and sellers alike: don’t chase a perfect scenario. Lower mortgage rates will make homeownership cheaper, trim payments, and ease long-term costs. But sitting idle waiting for “ideal” may mean missing current openings in a still competitive market.

As 2026 continues, watch those economic gauges, follow the Fed, and pay attention to local housing data. Optimism seems justified, but success often comes from acting wisely now rather than waiting endlessly for flawless conditions that rarely ever arrive.